Editor’s Note:

On November 29, the 36Kr WISE2024 summit was held in Beijing. 36Kr is one of China’s most influential business and technology media outlets, widely regarded as a key reference for understanding the evolution of China’s business environment.

At the summit, David He, Founder and Managing Partner of BA Capital, delivered a keynote speech titled "Eight Years in Consumer Investment: Structural Opportunities Are Creating Ample Market Space."

He noted that while the consumer market is undergoing broad transformations, it is also presenting structural opportunities. These include the resilient lower-tier markets, efficiency-enhancing business models, and the consistently growing demand for spiritual and experiential consumption. Concurrently, new trends are emerging, such as evolving consumer preferences and the substitution of international brands by domestic ones.

In his speech, David He also reiterated BA Capital's consistent investment methodology—the dichotomy between "experience-oriented" and "efficiency-oriented" models.

The following content has been translated from Chinese and edited for clarity and coherence.

Thank you to 36Kr for the invitation. The theme of this year's 36Kr WISE2024 summit is "Always With You," and I'd like to say that BA Capital has also "always been with you" in the consumer industry. Since our establishment in 2016, BA Capital has been investing for eight years, during which we have invested in about 40 companies, all within the traditional scope of consumer brands and retail enterprises.

Over these eight years, it is truly something to be grateful for that so many outstanding entrepreneurs have chosen to journey with us. Supporting exceptional consumer entrepreneurs and enhancing the value of consumption has always been our mission. Moving forward, BA Capital remains deeply passionate about the consumer industry and is committed to creating even greater value within it.

Today, I’d like to share BA Capital’s perspective on the consumer market and the opportunities we are focusing on.

First, what kind of consumer market are we in right now? Compared to the past two decades, the current market feels cooler—a sentiment many might share. However, this is not so-called "consumption downgrading"—the reason lies in the significant oversupply in the market. In this context, the quality of our consumption hasn’t downgraded, but oversupply has indeed led to price decreases, a trend supported by unit price statistics for most categories.

What about the state of consumers? In reality, consumers have never been easily defined by the purely rational "economic man" model in economics. Consumer confidence—expectations for the future—profoundly influences and shapes actual spending behavior. For consumers, a shift towards more conservative choices often has a stronger marginal impact on spending than actual changes in income. This means that even if real income hasn't decreased, weakened future expectations can make people more cautious, potentially exerting a greater influence on their actual consumption behavior.

However, we are not pessimistic about the environment. For both entrepreneurship and investment, China remains the world's second-largest single market, offering abundant structural opportunities and ample space for growth. Today, we want to share three of these opportunities:

1. The resilient and promising lower-tier markets.

2. Business models that enhance efficiency.

3. The continuously rising trend of spiritual and experiential consumption.

The Resilience and Potential of Lower-Tier Markets

In 2021, we conducted an in-depth survey in China's county-level regions. We visited ten counties, entered the homes of many local residents, and observed their daily lives from morning to night. It was from that time that we began to develop some understanding of the lower-tier markets.

At that time, this market received little attention from entrepreneurs and investors, yet it is an excellent one because of its sheer size—third-tier cities and below account for over 60% of China's population.

Almost all mass consumer goods companies follow a common pattern. In the end, the largest players usually dominate the markets where most people live, as seen in the U.S. and Japan. If the company hasn't established a solid foothold in its core and largest market, it will be difficult for it to become a true market leader.

In other words, if a mass consumer goods company focuses only on first- and second-tier cities, it is far from sufficient. Historical data shows that first- and second-tier cities contributed more to overall consumption growth for a long period, but new changes have emerged post-pandemic: these cities now show insufficient momentum in driving consumption.

In this context, the importance of lower-tier markets is self-evident. Firstly, demand-side stability remains strong: residents have relatively stable incomes, and, as mentioned earlier, consumer expectations—a key factor—are also relatively stable in lower-tier cities and county-level areas. Additionally, supported by recent national policies and county-centered urbanization, the population in county-level areas has continued to grow in recent years.

While demand-side stability in lower-tier and county-level markets has been improving, the supply side has seen limited qualitative upgrades, resulting in a clear supply-demand imbalance. In lower-tier markets, a common phenomenon is that some fast-moving consumer goods are cheaper in first- and second-tier cities. This is due to long retail distribution chains before goods reach consumers. For a long time, the needs of residents in lower-tier markets and counties have not been well met.

Against this backdrop, the emergence of higher-quality supply has fueled strong growth across various sectors in lower-tier markets. In recent years, most chain brands that have expanded to over ten thousand or even five thousand stores have successfully captured this market, using it as a core base for rapid nationwide expansion.

It is foreseeable that innovation on the supply side will present a long-cycle opportunity in lower-tier markets.

The essence of innovation is to improve efficiency. It means getting closer to users and lowering costs. Lower costs mainly come from two aspects: optimizing supply chain efficiency — by making better use of China’s large-scale supply chain and advanced manufacturing — and innovating business models to build more cost-efficient channels.

Efficiency Improvements from Business Models

In recent years, we have focused more on offline opportunities because structural changes have been happening in physical retail.

Online market share has grown in many categories, while offline share has declined. When offline share fell below a certain level, combined with changes in the macroeconomy, many traditional retail models were disrupted. This has been reflected in the performance and stock prices of department stores and supermarkets.

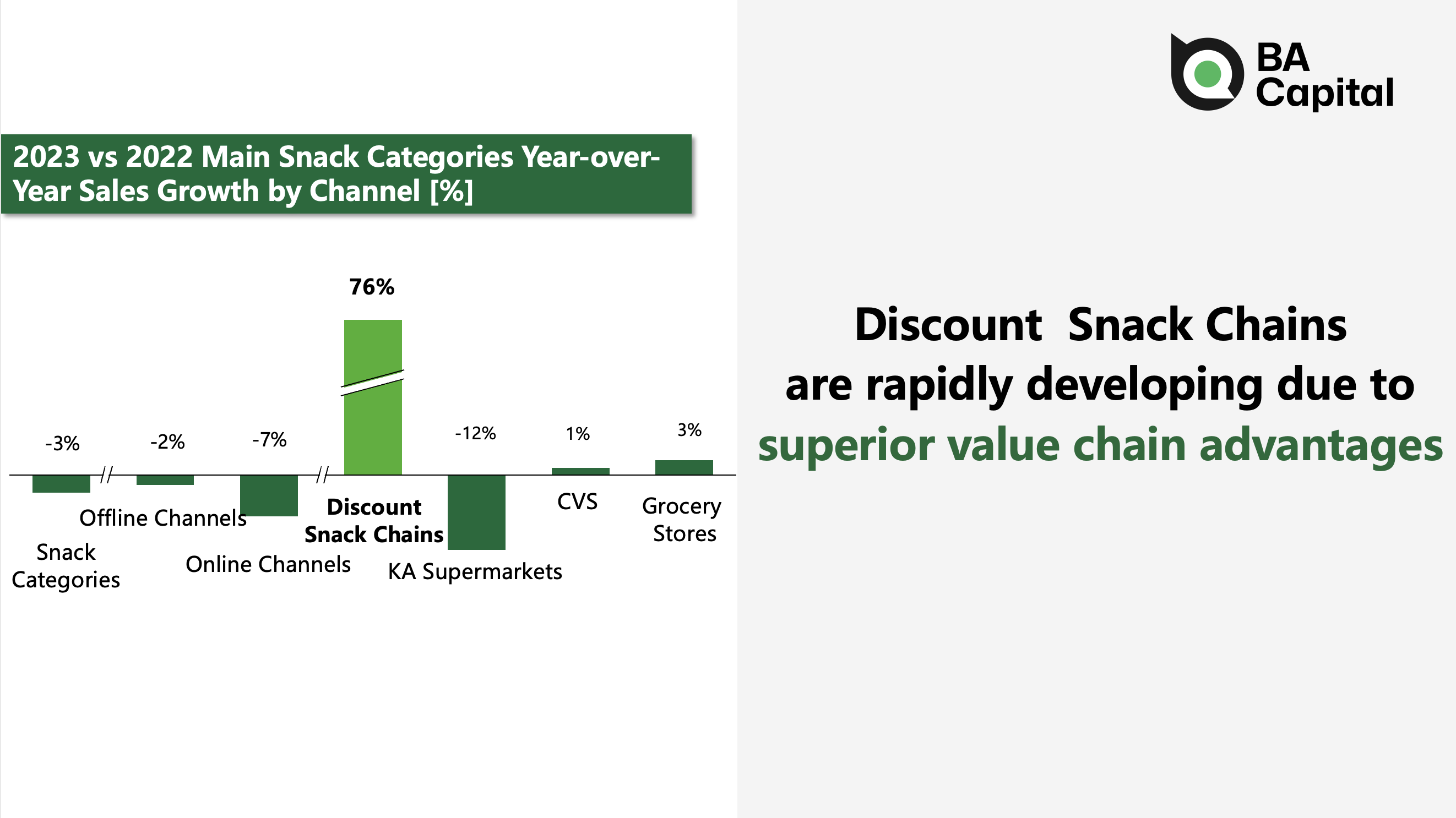

The opportunity in offline retail comes from shifts in channel traffic, which are reshaping the value chain. Some new business models have captured traffic from traditional hypermarkets. For example, discount retail formats, as an innovative business model in offline retail, are becoming an important trend.

In the future, discount retail will gradually become the mainstream of offline retail channels, with over 50% of retail models likely adopting discount retail business models. There are some divergences in how to implement discount retail models on the supply side.

We see models like Sam's Club, a membership-based warehouse store, meeting the needs of middle- and high-income consumers, while snack collection stores, such as our portfolio company Busy Ming Group, cater to mid- and lower-tier markets.

In the future, vertically integrated retail models, including multi-category and comprehensive categories, will emerge. Some of these companies may be new, while others may be traditional retailers that have successfully transformed. We have been closely watching the changes in traditional retail companies, supermarket chains, and department stores.

We are convinced that China's offline retail sector is poised to give rise to national champions with unprecedented market dominance. This is because past retail companies were often concentrated only in first- and second-tier markets or specific regions, which is insufficient given the scale of consumption in the Chinese market.

Some changes are already happening. Sam’s Club is growing rapidly. Discount snack chains have also become a remarkable offline model, expanding from zero to over ten thousand stores in a few years. Gains in operational efficiency have allowed these stores to deliver exceptional value to cost-conscious consumers in mid- and lower-tier markets, which in turn fueled rapid, explosive growth in demand. This is truly remarkable.

In addition, the market for unbranded product is also growing. It is important to note that unbranded product does not imply low quality. These products are often of very high quality, and consumers care less about brand attributes in these categories. Especially in mass, essential, and high-frequency categories, the market does not need a large number of brands. Consumers mainly want the best price, the best product, and the most convenient purchasing experience.

Unbranded product are excellent supply chain products, or products created through collaboration between supply chains and retail channels. This trend is more evident online, while offline channels have been focusing on reducing and optimizing SKU counts, improving product quality, and controlling costs. This is also expected to remain a major trend in the future.

The Continuous Rise of Spiritual and Experiential Consumption

Finally, I'd like to discuss a key investment focus we are highly focused on: "spiritual consumption" and "experiential consumption."

With the economic slowdown in recent years, some may question whether this focus is still worth pursuing. We believe opportunities exist, and we continue to dedicate significant time to tracking companies in this space and persistently researching user developments and changes within this sector.

As society develops and incomes rise, successive generations of better-educated young people are entering the workforce. With their deeper understanding of life, attention to spiritual needs—whether for companionship, self-expansion, or self-fulfillment—is increasing. Consumers’ willingness to spend on spiritual and experiential consumption is also growing, starting with the time they dedicate to these activities.

Today's youth are spending more time on spiritual consumption. The definition of "spiritual consumption" is quite broad: it could involve traveling, visiting exhibitions, purchasing a bottle of fragrance or scented candle, buying a collectible figure, watching a movie, or attending a stage play. People are willing to spend both time and money in these areas. Such spending does not necessarily imply high costs; these experiences are often cost-effective, providing meaningful and satisfying experiences for relatively modest expenses.

This could be a long-term entrepreneurial opportunity. It is not a highly saturated or intensely competitive sector where imitation quickly eliminates opportunities. Instead, it allows for significant differentiation, requiring entrepreneurs to invest deeply in product development, branding, and cultural content. Brands also need time to establish themselves with consumers, making time a true “friend” for entrepreneurs.

Let me give a few examples, such as our investment in POP MART. In the current environment of weakening consumer expectations, POP MART has not only maintained solid growth domestically but is also projected to achieve more than double its overseas revenue in 2024. The reason lies in people’s willingness to spend on products that may seem “useless.”

Some products have strong functional utility, while others may not appear "useful" for survival, yet they serve an important role in terms of consumer emotion and value recognition. We believe the market space for such products will continue to expand in the future.

Another example is Laopu Gold, which represents a new interpretation of traditional Chinese culture.

Using gold—a material highly favored by Chinese consumers—Laopu Gold has built a high-end jewelry brand with strong brand premium, exceptional user loyalty, and deep consumer affection. It has already established a presence in nearly all of China’s most premium shopping malls, an achievement that was nearly impossible for domestic jewelry brands in the past.

Brands like Laopu Gold may not have existed before, but will there be more in the future? We believe so, though it requires time to solidify.

Brands need to meticulously refine product craftsmanship, store design, and user service over the long term, while consistently adhering to a high-end positioning to construct a compelling brand narrative. A single misstep could lead to being abandoned by consumers. However, as long as brands persist in following this approach, we believe such companies will increasingly emerge in the future.

Outdoor sports is another investment focus we are very optimistic about in the long term, as it represents consumption that is highly spiritually oriented. Additionally, in categories such as pet supplies, coffee, food, skincare, and cosmetics, domestic brands are experiencing rapid growth, and the substitution of foreign brands is taking place widely.

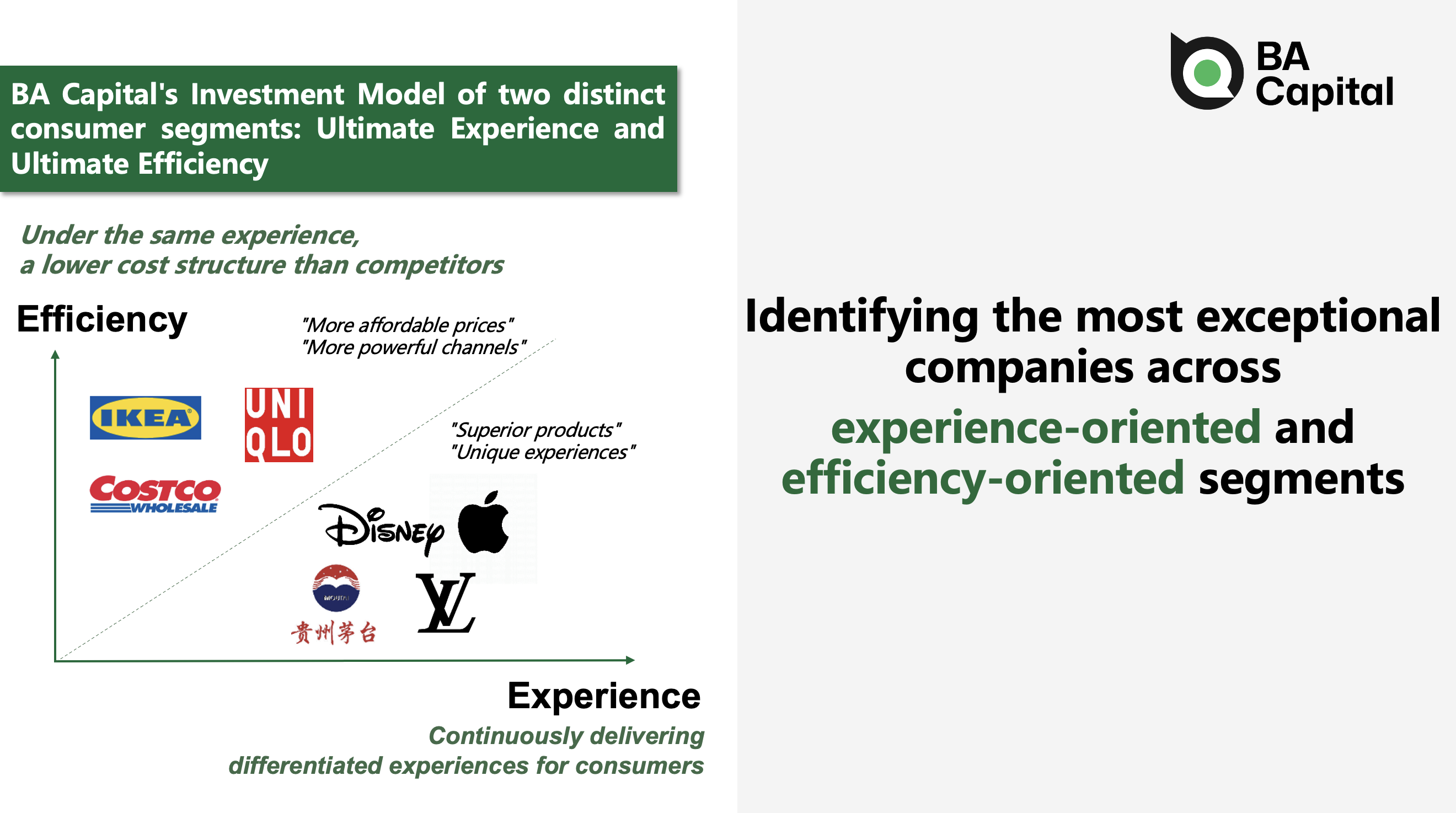

BA Capital's Investment Model in Consumer Investment

Furthermore, I’d like to share a perspective we have long held regarding consumer businesses. We continue to believe that the ultimate forms of consumer brands fall into two types: experience-oriented and efficiency-oriented.

In both entrepreneurship and investment evaluation, we make a strict distinction between these two types because they create very different kinds of value for consumers. Consequently, the value that entrepreneurs need to build also differs significantly. Efficiency-oriented businesses necessarily focus on lower costs and greater convenience, and their categories are generally basic, essential, and mass-market oriented. Experience-oriented businesses, on the other hand, require exceptional product content and strong differentiation.

However, consumers do not adhere to this. They do not only buy cheap products, nor only differentiated or expensive ones. In some scenarios, price takes priority, while in others, consumers may not even be able to accurately define what is expensive or cheap. Many outstanding companies never run promotions, and some even consistently raise prices over time.

But for entrepreneurs, it is crucial to identify their core capabilities from the very beginning. They also need to determine their company’s type, check if it matches consumer demand, and understand what to focus on at different stages. This is essential on the entrepreneurial journey.

Over the past eight years in consumer investment, although BA Capital has witnessed and navigated many market changes, we remain convinced that China’s consumer industry is vast and full of enduring opportunities.

Including amidst the current wave of overseas expansion, our advice to entrepreneurs remains the same: the “Home Market”—China—matters most. If you haven't established competitiveness in the Chinese market, you won't possess it overseas either; if you can perform well in the Chinese market, you certainly have the opportunity to do equally well overseas.

Finally, we want to emphasize that we will always be alongside entrepreneurs and the consumer industry. BA Capital will continue to be present in this field, seeking out and supporting generations of outstanding Chinese consumer enterprises. Thank you all.